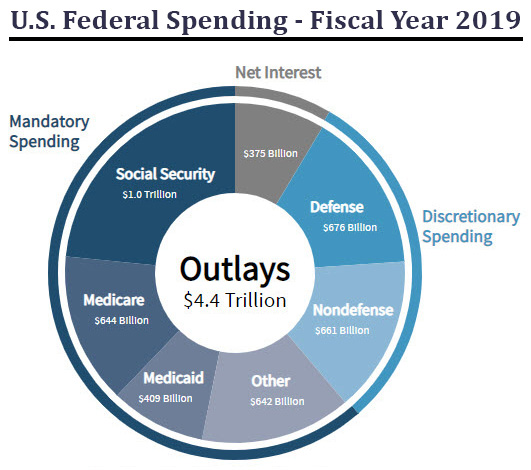

The sheer velocity of spending within the federal government is astounding (see pie chart graph below). In fiscal year 2019, the federal government spent about $4.45 trillion. That's $12 billion per day, $507 million per hour and $8 million per minute. By way of an example, James Gandolfini died with a $70 million net worth and his estate has had to pay about $30 million in federal and state estate tax. So, this $30 million tax payment was spent by the federal government in just under 4 minutes (a math calculation that is disconcerting to most people who have spent a lifetime creating a financial legacy).

Next, you need to think very carefully about what your estate tax is likely to be at your life expectancy (about age 85). Today, the estate tax exemption is $11,580,000 per person and the estate tax rate is 40% on any assets above the exemption. However, most commentators believe that the estate tax will be higher in future years for several reasons. First, the estate tax in the U.S. is at historic lows. Specifically, the average estate tax exemption in the U.S. tax code adjusted for inflation since 1915 is only about $1.5 million and the average estate tax rate over the last 104 years has been about 55%. By way of example, the estate tax exemption was only $675,000 as recently as the year 2000. Second, the current tax law (Tax Cuts and Jobs Act of 2017), provides that the estate tax exemption will decline to about $6 million per person starting in calendar year 2026. Third, the United States now has the largest federal debt in history with no end in sight.

Based on these factors, our recommendation for most clients when creating financial models and forecasts is to assume a $3.5 million exemption and a 50% estate tax rate unless their estates are $50 million or more. In that case, we recommend just assuming an estate tax of 50% of the client’s projected net worth (as we expect the exemption to be phased out for larger estates at some point in the future). When we go through this math, most clients and their advisors indicate that these assumptions are reasonable (if not optimistic on our part). One other thing to consider is that the estate tax is due within 9 months of death. As a result, there could be additional losses to the estate caused by the forced sale of estate assets.

So, is there any way to avoid this massive destruction of family wealth? The answer is yes and we can help you implement planning solutions that will substantially reduce or completely eliminate the negative impact of the estate tax.

2. What To Do?

One effective way to eliminate the estate tax is to set up your estate documents so that all of your wealth that exceeds your remaining estate tax exemption is given to charity. For simplicity, let’s use an example where at the time of the client’s death, he has a $50 million estate and an estate tax exemption of zero. In this case, the client could leave their entire $50 million estate to charity and pay zero tax. For many clients, this solves the estate tax problem and essentially converts taxes into charitable donations.

However, in many cases, our clients want to leave some or all of their wealth to their children, extended family or friends (known as “non-charitable estate beneficiaries”). In that case, assuming the client wants to leave their entire $50 million estate to their children, then the estate will pay about $25 million in taxes and distribute a net of about $25 million to the kids.

So, how can we improve this situation when the client wants their wealth to go to non-charitable beneficiaries?

Our solution is for the client to purchase a life insurance contract with a $25 million death benefit. The policy will be owned by an irrevocable life insurance trust so that any death benefits ultimately paid are outside of the client’s estate (free from any income or estate tax). Now, upon the death of the client, the full $50 million estate goes to a family foundation that is qualified as a charity. The net result is that $25 million goes to the children (the same amount they would have received under the status quo) plus the family controls a charitable foundation with a $50 million fund balance. Each year, the cash in this foundation is invested and then there are rules about how much must be donated each year from the foundation to other charitable organizations. Clearly, most families would prefer to have control over $75 million in assets versus only $25 million with the status quo.

As an alternative to the family foundation structure described above, some families just use the $25 million in life insurance proceeds to pay the estate taxes. This then results in the entire $50 million estate transferring to the family members free and clear. This approach is common when the family wants to keep business assets intact for the next generation and does not want these business assets to go into the family’s charitable foundation.

3. How Do We Fund The Life Insurance Policy?

To fund the life insurance policy, there are a number of different strategies depending on the facts and circumstances of each client. Factors such as estate size, liquidity, asset types, projected asset growth, control considerations and family dynamics are crucial elements.

For smaller transactions, it’s relatively easy to just make cash gifts to an irrevocable life insurance trust. That said, these cash gifts for premium can cause gift tax problems over time (especially with larger estates). So, one strategy that often makes sense is to use grantor trusts. In a typical example, the client sells assets at a discount to the trust and takes back a seller note which accrues interest at the Applicable Federal Rate (“AFR”). Next, the client makes loans to the trust equal to the life insurance policy premium (which also accrues at the AFR). Then, if the sold assets appreciate faster than the AFR, this creates growth assets outside the estate that can be used to pay back the client’s seller note and premium loans without ANY gift from the client to the trust. We like this strategy for clients that have very large estates ($50 million or more) and where the client:

is somewhat risk averse and doesn’t like popular strategies such as premium financing discussed below (where in order for the plan to work, the long term market returns must average at least 200 to 300 basis points above the long term borrowing costs);

has sufficient liquidity to pay the scheduled policy premiums;

has private equity, public securities or real estate that are likely to grow faster than the AFR in future years.

Note: Currently, the long term AFR is only about 1% per year (the lowest in history) making the grantor trust described above one of best estate tax reduction strategies available today.

As mentioned above, another popular method of funding life insurance premiums on a trust owned life insurance policy involves “Premium Financing Life Insurance” or “PFLI”. Let’s explain this a little more. About 30 years ago, some financial analysts figured out that there could be some interesting ways to fund life insurance using leverage if you were willing to commit to a program of long-term investing. They further theorized that since life insurance for estate tax planning is typically “long term” with policies funded until the future life expectancy of the client, this could present some interesting opportunities. This gave birth to the premium financing marketplace and PFLI.

The fundamental principal is that long term market returns tend to be higher than long term borrowing costs. Specifically, investing in the S&P index over time would typically give you a return of 7% to 10% (depending on whether you are reinvesting the dividends). You can test this at the website below:

So, if you could borrow money over the long term at 4% or 5%, then you would earn more in the market than you were paying out in interest to the bank (“leverage profits”). And, that’s basically what people are doing when they buy stocks on margin. With PFLI, the third-party bank’s loans are reinvested in the life insurance contract which invests the money in the S&P index fund (or alternative stock index). What’s different with PFLI is that the leverage profits are used to fund the mortality costs of the life insurance policy. This is significant because the policy is outside of the client’s estate so the death benefits ultimately paid are both income and estate tax free. Under current law, the leverage profits are not considered gifts and therefore never taxable to the estate. And, that’s a big deal from a “net after-tax return on investment” point-of-view when the alternative is a 40% to 50% estate tax.

Essentially, the PFLI structure allows the wealthy client to utilize low interest bank financing and collateral to fund the cost of the large amounts of tax free death benefits outside their estate. The gamble is that the equity returns will outperform the borrowing costs. And, that IS an unknown. So, you don’t put all your eggs in this PFLI basket. However, to put some money into this transaction may be advisable for certain wealthy families (given the limited downside risk, low interest rate environment and substantial upside potential with equity returns funding income and estate tax free policy death benefits). Finally, the equity index inside the life insurance contracts are designed with caps at around 10% and a floor of 0% (further reducing the risk of down markets and creating a higher likelihood of equity returns that are greater than the long-term borrowing costs).

One last comment. If you analyze long term periods of time (more than 20 years), there has never been a time in the past 100 years when long-term market returns were not substantially higher than long-term borrowing costs. While comforting, what happens if the client dies prematurely before the equity fund has had a long enough time to increase the probability that it will grow at a higher rate than the long-term, fixed interest cost? Well, that’s no problem. If the client dies early, there’s an even bigger windfall to the family since the death benefits of the policy are now paid early, on a much smaller cumulative premium outlay. Of course, early death isn’t such a good result for the client so we encourage them to live as long as possible. Sorry, this stuff is pretty dry without some humor thrown in here and there.

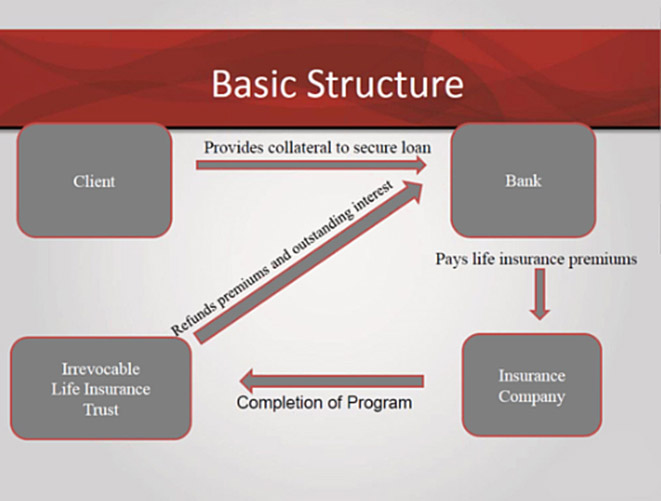

As a consequence of these tax advantages, the premium financing industry has grown rapidly since 2000. Now, thousands of wealthy families have implemented the PFLI strategy to get wealth to heirs without estate tax and then leave their taxable estates to family foundations or charity. Shown below is a flowchart on the basic PPLI structure.

4. Next Steps

If any of the concepts described above sound interesting to you, contact us. We will then schedule a short 20-minute phone call to ask a handful of questions about your financial assets and personal situation. Then, with your permission, we will run cash flow models showing how your estate will grow or shrink in the future using different growth and tax assumptions. These models will also give us information about what, if any, future tax might be owed by your estate upon your death. We will then review this information with you and suggest different tax mitigation strategies that could be useful. If you like any of the suggestions we make, then our tax attorneys typically work with your existing estate planning attorney to discuss our ideas and how they might integrate into your existing estate plan. Of course, if you don't have an existing estate planning attorney, then we can recommend one in your area that will exclusively represent your interests during this process. For clients with current net worth over $20 million that have not implemented the types of tax mitigation strategies we recommend, we can typically show a 200% to 500% increase in net after tax wealth under family control when compared with just having a garden variety pour-over will, living trust and taxable estate.

One last thing. When applying for large death benefit amounts for new life insurance policies (over $20 million), the reinsurance market is crucial and can impact how much life insurance is approved as well as how much you are charged each month for the insurance policy. Our reinsurance partners have placed more high net worth life insurance than any other organization in the marketplace and this means that we can deliver the best offers to you. Call us to learn more.

PROTECTING YOUR ESTATE

PROTECTING YOUR ESTATE